As climate change becomes a major concern for millions of savers, The Shift Project‘s Observatory 173 Climate – Life Insurance submits several key questions that must now be answered by French life insurers, notably on their coal investment policies.

Reports 173, Year II: French life insurance investment policies under the microscope

The Observatory 173 Climate – Life Insurance was created by The Shift Project in 2016 to monitor the implementation by life insurance in France of Article 173 of the Energy Transition Act[1], which requires financial portfolio managers to explain how they take into account (or not) the climate issue in managing their assets.

This law provides for annual reporting by institutional investors on their climate-related risks, as well as on their investment policy to address them.

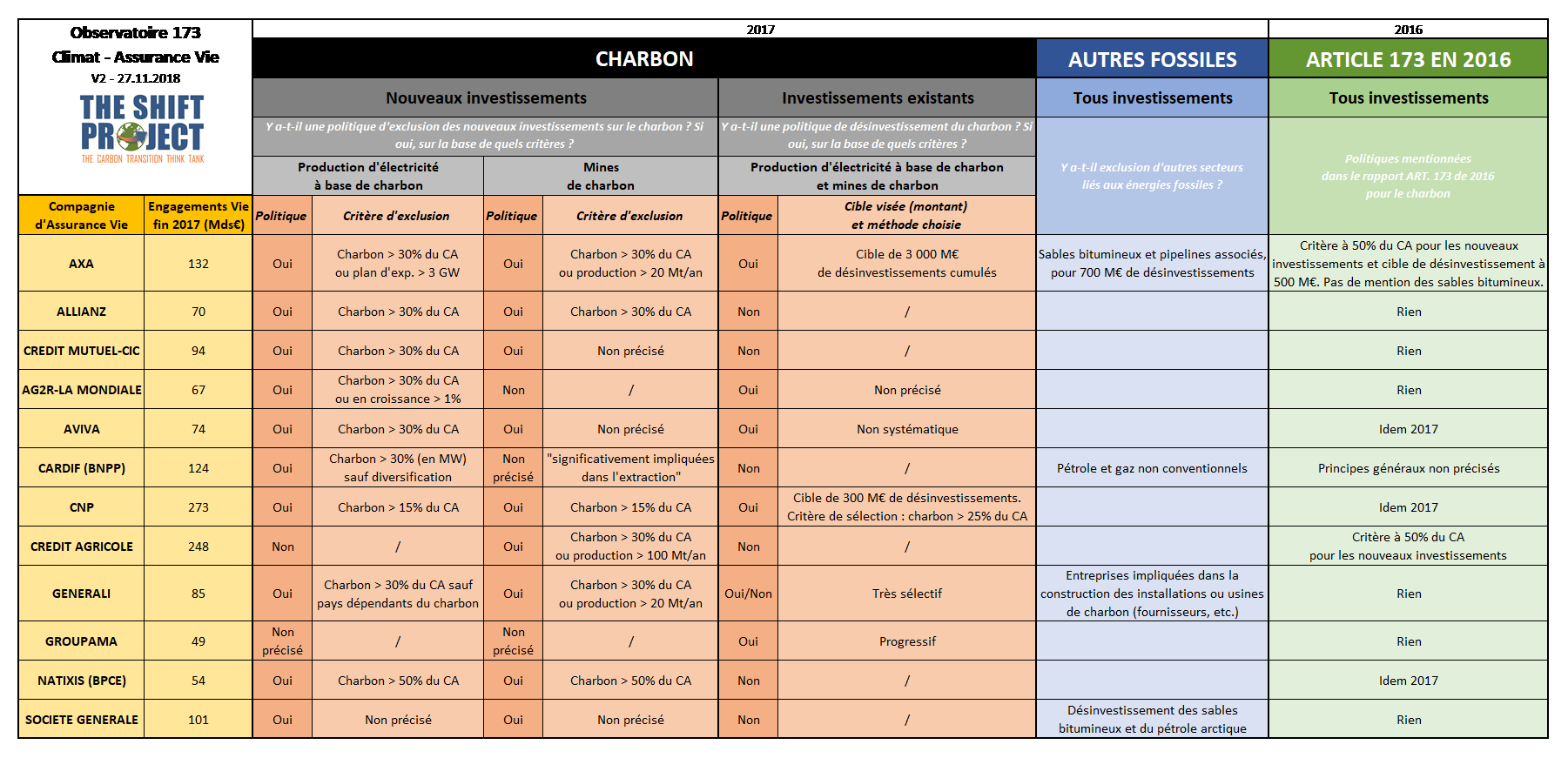

The Observatory 173 produced its first report in 2017, based on the publications of the twelve largest French life companies, which alone manage nearly a third of the financial savings of the French (with more than 1300 billions euros).

In 2018, the analysis focused on coal investment strategies. While a review of the application of the provisions of Article 173 of the law will be carried out by the government before 31 December 2018, the Observatory 173 publishes the first analysis of coal exclusion policies in the investments of French life insurance companies.

Why and how not to go to coal?

A global consensus seems to be emerging to consider coal-related sectors as deserving special vigilance. For many stakeholders, it would be imperative to exclude certain coal investments from now on: on the one hand, coal mining (mines), and on the other hand, coal-fired power generation (power plants).

The Observatory 173 analysed in detail the policies of the twelve main French life insurance companies. It noted a strong increase in the selective exclusion of investments. These exclusion policies are detailed in the report.

After the publication of an alarming IPCC special report on the somewhat illusory “target” of 1.5°C[2], the issue of coal investment appears critical, criticizable and criticized.

Observatory 173 addresses the issues of the underlying objectives of the coal exclusion policies of French life insurers. Are exclusion policies part of an individual approach or a collective ambition? Is it herd behaviour or the result of an autonomous reflection? Are some actions in practice just plain green washing? Do investors have a clear idea of their initial situation? Do they act consistently for other carbon energies? Do they have a strategy regarding scope extensions already imagined or even planned? Are they sometimes in a conflict of interest situation? Have they identified reputational or judicial risks? Finally, do life insurers properly educate the general public about their strategy, when they have one?

What if the “stranded assets” approach was stranded?

The 2016 speech by Bank of England Governor Mark Carney to the financial industry made the term “stranded assets” famous. This term refers to assets that are highly dependent on fossil fuels, which may therefore be significantly or totally devalued during the energy and climate transition. There is currently a broad consensus that coal-related industries (and in particular coal mines and coal-based power plants) could become the main source of “stranded assets”. However, are the prospects for lower returns on these assets well founded ? This is not obvious today, when we observe the rise in coal prices, and the refusal (Australia) or inability (Germany, etc.) of several major economies to quickly turn away from its exploitation.

Should the rationale for coal exclusion policies therefore come from a search for profitability (the world turning away from coal, these assets would be less valuable), or from an ethical choice made at the expense of profitability? Another sensitive issue is how to ensure that an exclusion effectively hinders the continued operation of the asset concerned. Should we consider an alternative investment strategy: remaining a shareholder in a coal company in order to change its corporate strategy from the inside, even if it means that the company’s profitability drops?

Given the growing importance of the issue of coal exclusion from investments, and the growing sensitivity to the issue of climate change for millions of French people who have entrusted their savings to life insurers, the Observatory 173 asks them to provide more explanations on the justification for their decisions and to better explain their energy transition strategy.

[1] Act No. 2015-992 of 17 August 2015 on the energy transition for green growth, on https://www.legifrance.gouv.fr/affichTexte.do?cidTexte=JORFTEXT000031044385&categorieLien=id (online)

[2] Summary for Policy makers – IPCC special report on the impacts of global warming of 1.5°C above pre-industrial levels and related global greenhouse gas emission pathways, in the context of strengthening the global response to the threat of climate change, sustainable development, and efforts to eradicate poverty, on http://report.ipcc.ch/sr15/pdf/sr15_spm_final.pdf , October 2018

Contact

Michel Lepetit – Pilote de l’Observatoire 173 et Vice-Chairman, The Shift Project

Mobile : +33 6 03 26 93 18 | E-mail : michel.lepetit@theshiftproject.org

This project is dedicated to our friend Christophe Point